How to Avoid Probate in Arkansas

Jul 15, 2025

When you hear the word "probate," what comes to mind? For most people, it sounds complicated, expensive, and frankly, a little intimidating. And they're not wrong.

Probate is the official, court-supervised process for handling someone's estate after they pass away. If there’s a will, the court's job is to make sure it's valid and that its instructions are followed. If there isn't a will, Arkansas law steps in to decide who gets what.

Here's the twist most people don't see coming: having a will doesn't let you avoid probate. It actually guarantees it. The will becomes the instruction manual for the court, kicking off the very process many hope to sidestep. This is precisely why so many Arkansas families make it a priority to plan around probate. The reasons are practical, personal, and have a real impact on the people you leave behind.

What Is Probate and Why It Matters in Arkansas

The Real-World Costs of Probate

The biggest headaches with probate aren't just the legal hoops you have to jump through. They're the tangible hits to your family's time, money, and privacy. The process isn't free, and those costs can pile up fast, chipping away at the inheritance you worked so hard to build.

Common expenses include:

Court Filing Fees: Every case starts with a fee paid to the county circuit court.

Attorney's Fees: These are often calculated as a percentage of the estate's total value or billed by the hour.

Personal Representative Fees: The person in charge of managing the estate is entitled to compensation for their work.

Appraisal and Bond Costs: You might have to pay to get property professionally valued or to purchase a bond that insures the estate.

Think about a family in Fayetteville trying to settle a loved one's affairs. While they're grieving, these fees are quietly draining the estate, leaving less for the people it was intended for.

Probate is a public affair. Every single document filed—the will, a list of assets, any debts, and who the beneficiaries are—becomes part of the public record. Anyone can walk into the courthouse and look up the financial details of your family.

Significant Delays and Loss of Control

Time is another huge issue. The probate process in Arkansas simply isn't fast. By law, an estate has to stay open for at least six months. This gives potential creditors a chance to come forward and make claims. But that's just the minimum.

It’s not uncommon for cases to drag on for much longer.

A simple disagreement between heirs or a challenge to the will can easily stretch the process to a year or more. During that entire time, your family might not be able to access their inheritance. They can't sell the house or the car. This can create a massive financial strain, especially if they were counting on those assets for support.

If you ever find yourself responsible for handling an estate, it’s critical to understand the steps involved. To get a clearer picture, take a look at our comprehensive guide on https://arkansaslegalnow.com/articles/a-complete-guide-to-how-to-probate-an-estate-in-arkansas.

The Emotional Toll on Your Loved Ones

Beyond the money and the long waits, the probate process itself can create a lot of unnecessary stress and conflict. Having family finances laid bare for the public to see can spark arguments or attract unwanted attention. The rigid, formal nature of the court system just adds another layer of anxiety during an already painful time.

By planning to avoid probate, you're doing more than just saving money and time. You’re giving your family the gift of privacy and peace of mind. You’re ensuring they can grieve without the added pressure of a drawn-out, public court battle. Even when probate is unavoidable, taking the right steps can make a world of difference. This After Death Checklist to Simplify Probate is a great resource to help ease that burden.

Using a Revocable Living Trust to Keep Control

When people ask me for the most powerful and flexible way to sidestep the court system entirely, my answer is often a Revocable Living Trust (RLT). It’s an incredibly effective strategy that lets you keep full control over your property during your lifetime, then pass it directly to your loved ones without a judge’s involvement after you’re gone.

Think of a living trust as a private legal rulebook you create for your assets. You set it up, and then you transfer ownership of your valuable property—like your house or investment accounts—from your personal name into the trust's name.

You remain in the driver's seat as the grantor (the creator), the trustee (the manager), and the beneficiary (the one who benefits). Nothing really changes in your day-to-day life. You can still sell your house, refinance your mortgage, or manage your investments just like you did before.

The "revocable" part is what makes it so flexible. It simply means you can change your mind. You can amend the trust, add or remove assets, or even dissolve it completely whenever you want.

How a Living Trust Works in the Real World

Let's walk through a practical example. Imagine a couple from Little Rock, John and Mary. They own their home, a joint bank account, some stocks, and a small vacation cabin near Greers Ferry Lake. Their main goal is simple: make things as easy as possible for their two adult kids down the road.

If they did nothing, all those assets would be tied up in the Arkansas probate court. Instead, they work with an attorney to create the "John and Mary Smith Revocable Living Trust."

Here’s what happens next:

Their Home: A new deed is prepared and filed, transferring ownership from "John and Mary Smith" to "John and Mary Smith, Trustees of the John and Mary Smith Revocable Living Trust."

Bank Accounts: They go to their bank and simply retitle their checking and savings accounts into the trust's name.

Investments: They instruct their financial advisor to change the owner of their investment portfolio to the trust.

Legally, the trust now owns everything. But since John and Mary are the trustees, they manage it all just like before. The real magic happens when they pass away. Their daughter, who they named as the successor trustee, takes over automatically.

She doesn't need to ask a court for permission. She just follows the private instructions laid out in the trust document to settle any final bills and distribute the property directly to herself and her brother. The entire process is private, quick, and completely avoids probate.

A living trust does more than just avoid probate—it protects you during incapacity. If you become too ill or injured to manage your finances, your chosen successor trustee can step in immediately to pay your bills and handle your affairs. This avoids a costly and public guardianship proceeding in court.

Funding Your Trust Is Non-Negotiable

Just creating the trust document isn't enough. I've seen it happen too many times: someone goes through the trouble of setting up a trust but then fails to take the final, most important step.

Funding the trust—the act of actually retitling your assets into its name—is what makes it work. An unfunded trust is like an empty vault. It exists on paper, but it doesn't protect anything. Your successor trustee can only manage assets the trust actually owns. Anything left out will probably end up in probate, defeating the whole purpose of your planning.

Choosing Your Successor Trustee Wisely

The person you name to manage your trust after you're gone holds a huge amount of power and responsibility. They will be in charge of protecting and distributing your life's savings according to your wishes.

Think carefully when making this choice. Consider:

Trustworthiness: This is the absolute most important quality. Pick someone with rock-solid integrity.

Financial Savvy: Are they responsible with their own money? They'll need to be responsible with yours.

Willingness: This is a real job that takes time and effort. Make sure they are actually willing and able to take it on.

It’s always a smart move to name at least one alternate successor trustee, just in case your first choice can't serve for any reason.

Trusts are one of the oldest and most reliable tools for avoiding probate, and living trusts have become incredibly popular because they keep your affairs private. That’s a massive advantage, as probate is not only public but can also be expensive, sometimes eating up to 6% of an estate’s value in fees. It's also slow—the process in Arkansas takes a minimum of six months. To learn more about how these and other tools work, you can review this overview of probate avoidance strategies in Arkansas.

The Pros and Cons of Joint Ownership

On the surface, adding another person to your property titles seems like a genius move to dodge probate. And sometimes, it is. The strategy hinges on a specific form of ownership called Joint Tenancy with Right of Survivorship (JTWROS).

When you own property this way, your share automatically and instantly passes to the other joint owner when you die. It’s a direct transfer.

The asset—whether it’s your home, your car, or a bank account—never becomes part of your probate estate. It completely sidesteps the court process, which means a fast and seamless handover. You don't need a will or trust to pass on that specific asset because the deed or account agreement already lays out exactly what happens next.

How Joint Ownership Works in Practice

Think about a common Arkansas scenario. An aging mother in Hot Springs wants her son to inherit her house without any legal fuss. She meets with an attorney to draw up a new deed, listing both of them as "joint tenants with right of survivorship."

Fast forward a few years. When she passes away, the house immediately becomes her son’s sole property. He doesn't have to ask a judge for permission or wait for a court order. His only task is to file a copy of his mother's death certificate with the county land records to get a clean title. It's an incredibly clean and efficient method for this one goal. The same idea applies to joint bank accounts, which pass right to the surviving owner.

This simplicity is by far the biggest selling point of joint ownership. But this easy path is also littered with serious potholes you absolutely have to know about before you add anyone's name to your property.

While joint ownership is a powerful tool for avoiding probate on a specific asset, it is not a complete estate plan. It only affects the assets that are jointly owned and does nothing to address your other property or plan for incapacity.

The Hidden Risks of Adding a Co-Owner

Here’s the catch: when you add someone who isn't your spouse as a joint owner, you’re giving them an immediate ownership stake in your property. That means you are no longer the sole decision-maker.

Want to sell the house or refinance the mortgage? You now need your co-owner’s signature.

Even more frightening, you’re also hooking your asset to their financial life.

Creditor Claims: If your new co-owner gets sued, files for bankruptcy, or racks up unpaid tax bills, their creditors could slap a lien on the property—your property.

Divorce Proceedings: Should your co-owner go through a divorce, their share of your property could be classified as a marital asset. Suddenly, your home could be dragged into their legal drama.

Loss of Control: Once you add someone to the title, you can't just take them off. That decision is nearly impossible to reverse without their full cooperation.

Unintended Tax and Family Consequences

Putting a child or other non-spouse on your deed can create some unexpected tax headaches. The IRS might see adding your child to the deed of your home as a major gift. If the value of their share is more than the annual exclusion amount, you could be on the hook for filing a gift tax return.

Finally, think about your family dynamics. Let's say you have three kids, but you only add one to the deed of your home to keep things "simple." Legally, that one child inherits the entire property. The other two get nothing, no matter what your will says about dividing everything equally.

This can breed resentment and spark ugly family feuds, completely wrecking your true intentions. Joint ownership can be a handy tool in the right situation, but its simplicity hides serious risks if you're not careful.

Of all the ways to keep your estate out of probate court, this might be the easiest and most powerful strategy hiding in plain sight. Many of your most valuable assets already have a built-in feature that lets you pass them directly to your loved ones, completely bypassing the court system. This is done through beneficiary designations.

These simple forms—often just a single page or a few clicks online—are essentially a contract between you and a financial institution. They act as a direct order, telling the bank or brokerage firm exactly who should receive the asset when you pass away. Because this transfer is handled by contract, the asset never becomes part of your probate estate. It's a clean, direct handoff.

The Power of POD and TOD

Here in Arkansas, the two most common types of these designations are Payable-on-Death (POD) and Transfer-on-Death (TOD). They function almost identically but apply to different kinds of assets.

Payable-on-Death (POD): This is for your liquid cash accounts. Think checking accounts, savings accounts, money market accounts, and certificates of deposit (CDs). You simply fill out a form with your bank naming a POD beneficiary.

Transfer-on-Death (TOD): This is for securities, like your stocks, bonds, and brokerage accounts. Arkansas law also allows for TOD registration for motor vehicles, which is a fantastic way to make sure a car or truck passes to an heir without getting stuck in probate.

The real beauty of these tools is their simplicity and flexibility. You remain the sole owner with total control during your lifetime. The person you name as beneficiary has zero rights to the asset while you're alive. You can change your beneficiary anytime you want by filling out a new form, and it costs nothing.

A Real-World Annual Financial Review

Let's look at a practical example. Imagine Sarah, a teacher in Conway, who carves out one afternoon each year to review her finances. Her goal is to ensure her plan still reflects her wishes and that she’s using every tool available to avoid probate for her family.

First, she logs into her online banking portal. She clicks through to her main checking and savings account settings and finds the "Payable-on-Death Beneficiaries" section. She sees she named her son as the primary beneficiary years ago. That’s still correct, but she decides to add her sister as a contingent beneficiary—a backup—just in case her son can't inherit for any reason. This takes her less than five minutes.

Next, she opens her retirement account dashboard. Her 401(k) and Roth IRA are her largest assets. She pulls up the beneficiary information for both and confirms her son is still listed as the primary. Since these are retirement accounts, getting the beneficiary right has major tax implications, making this check-up even more critical.

Finally, she remembers her life insurance policy. Years ago, she'd named her ex-husband as the beneficiary. Since their divorce, she never thought to change it. With a quick phone call and an e-signature, she updates the policy to name her son instead, preventing a massive and irreversible mistake. In under an hour, Sarah has effectively shielded her biggest assets from the probate process.

Crucial Tip: Never, ever assume your will can override a beneficiary designation. It can't. That beneficiary form is a legal contract that your bank or brokerage firm must follow, no matter what your will says. If your will leaves everything to your daughter but your old 401(k) still names your ex-spouse, your ex-spouse gets the money. Period.

Now is a great time to take stock of the various probate avoidance methods available to Arkansans. This table breaks down the most common strategies to help you see how they compare.

Probate Avoidance Methods at a Glance

This table compares the most common probate avoidance strategies, outlining their key features, benefits, and potential drawbacks to help you decide which is right for you.

Strategy | Assets Covered | Primary Benefit | Key Consideration |

|---|---|---|---|

Living Trust | Virtually all assets (real estate, bank accounts, investments, etc.) | Comprehensive control and privacy; avoids probate for all trust assets. | Higher upfront cost and administrative effort to set up and fund. |

Joint Ownership | Real estate, bank accounts, vehicles. | Simple to set up; asset automatically passes to the surviving owner. | The joint owner has immediate rights; can expose assets to their creditors. |

Beneficiary Designations | Bank accounts (POD), securities (TOD), retirement accounts, life insurance. | Very easy and free to implement; assets transfer directly to the beneficiary. | Must be reviewed regularly; can't be overridden by a will. |

Small Estate Affidavit | Personal property up to $100,000 (excluding liens). | A simplified, faster, and cheaper alternative to full probate for small estates. | Only applies to estates below the legal limit and can't transfer real estate. |

Each of these tools has its place in a well-rounded estate plan. For many people, a combination of these strategies provides the most effective and affordable protection against probate.

Keeping Your Designations Current

Sarah’s annual review makes an essential point: beneficiary designations are not a "set it and forget it" task. Think of them as living documents that have to be reviewed and updated after any major life event.

You should pull up your forms and double-check them immediately after:

Marriage or Divorce: This is the #1 reason for catastrophic and costly errors.

Birth or Adoption of a Child: You may want to add a new child or set up a trust for their benefit.

Death of a Beneficiary: If your primary beneficiary passes away and you haven't named a backup, the asset will probably end up in probate after all.

A Major Change in Relationships: If you have a falling out with someone you named as a beneficiary, you'll want to update your forms right away.

Taking a few moments to review these simple forms is one of the most effective things you can do to make life easier for your family. It’s a guaranteed way to keep some of your most significant assets out of court, saving your loved ones time, money, and a world of unnecessary stress.

Using a Small Estate Affidavit in Arkansas

Let's talk about a fantastic tool for smaller, more modest estates in Arkansas. Not every family needs to get tangled up in the long, formal probate process. In many cases, the law offers a much simpler and faster alternative: the Affidavit for Collection of Small Estate.

Think of it as an efficient shortcut designed to save families a ton of time, money, and headaches when the situation is right. It allows heirs to collect a deceased person's property without ever having to step foot in a courtroom. It's a powerful option, but it isn't for everyone. You have to meet some pretty specific rules to use it.

Is Your Estate Eligible?

Before you even think about drafting an affidavit, you have to be certain the estate qualifies under Arkansas law. The two most important factors are the estate's total value and how long it's been since your loved one passed away.

Here are the hard and fast rules:

Maximum Value: The total value of the estate, after you subtract any liens and encumbrances (like a mortgage or a car loan), cannot be more than $100,000.

Waiting Period: You absolutely must wait at least 45 days after the person's death before you can use this affidavit.

No Real Estate: This process is only for collecting personal property. That means things like bank accounts, vehicles, and household items. You cannot use it to transfer ownership of a house or land.

If the estate checks all these boxes, you're in a great position to move forward. The affidavit is basically a sworn statement where you, as an heir, declare that you're entitled to the property. For a more detailed breakdown, we’ve put together a guide on unlocking the mysteries of small estates in Arkansas that really digs into the specifics.

The Collection Process Step-By-Step

Okay, so you've confirmed the estate is eligible. Now what? The process itself is refreshingly straightforward. It really just comes down to getting the right form, filling it out correctly, and getting it legally validated.

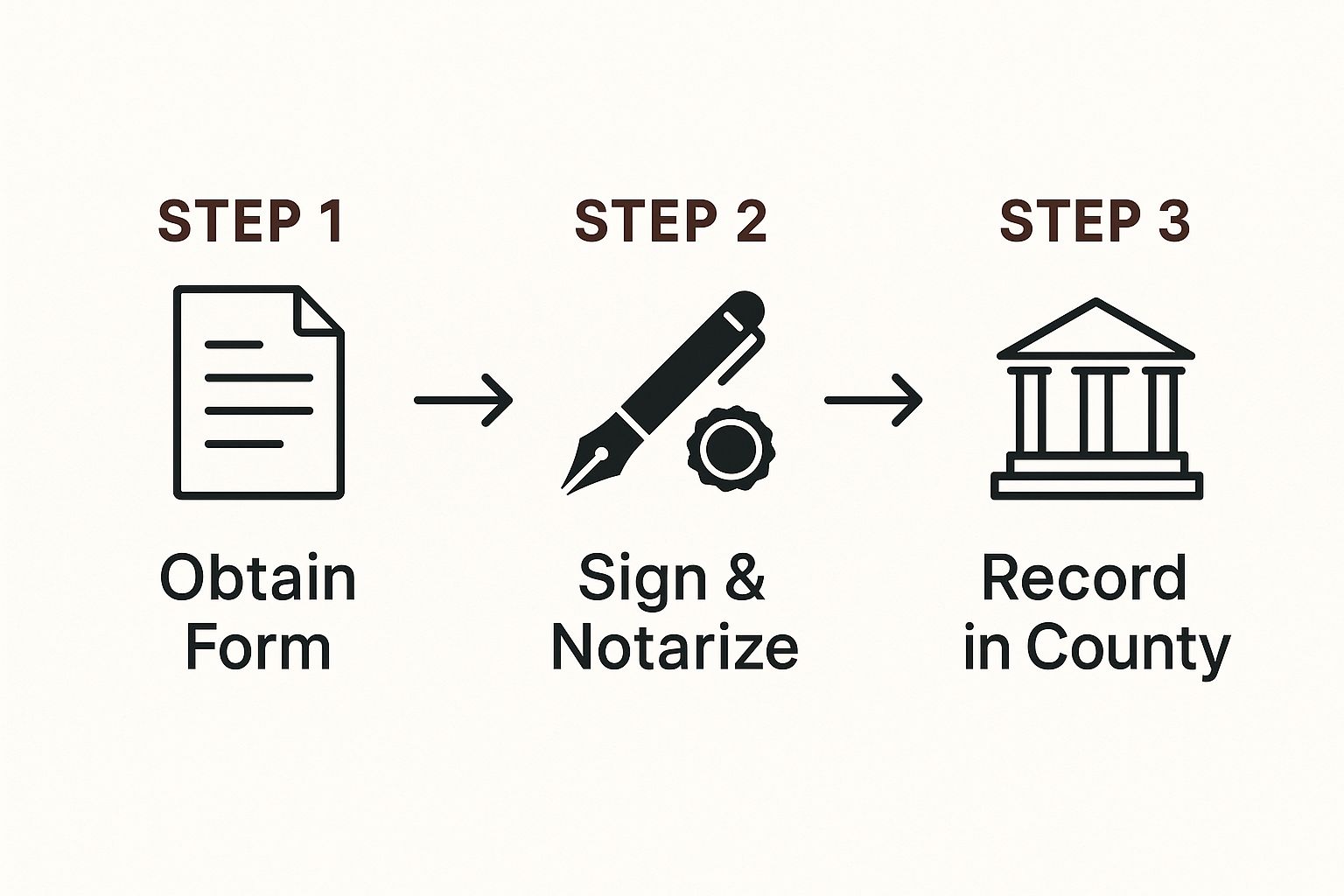

This visual guide breaks down the simple, three-part process for filing the affidavit.

As you can see, it highlights the essential flow: get the form, get it notarized, and get it recorded.

Once you've done that, you need to prepare your documents for presentation. You'll need to attach a copy of the death certificate to your signed and notarized affidavit. You'll also need to bring along a copy of the affidavit that has been filed and stamped by the circuit clerk. With this packet of documents in hand, you can go to any institution holding the assets, whether it's a bank or the DMV.

Key Takeaway: Upon receiving your properly completed and filed affidavit, the bank or other institution is legally required to release the property to you. This protects them from any further liability and makes the transfer secure and official.

Let's walk through a real-world example. Say you're trying to access your mom's checking account, which has $5,000 in it. You would take your filed affidavit and her death certificate to the bank. The bank staff will review the documents, close the account, and hand the funds over to you.

Just like that, you've avoided court hearings, expensive legal fees, and the months-long waiting game of formal probate. It's an ideal solution for many Arkansas families dealing with a smaller estate.

Common Questions About Avoiding Probate

It's completely normal to have questions pop up, even after you’ve put together a solid plan to keep your estate out of probate. Estate planning can feel like a maze, but getting clear on a few common points will give you the confidence you need to protect your family. Let's walk through some of the questions we hear most often from Arkansans.

One of the biggest myths we have to bust is the idea that just having a will is enough to avoid probate. In reality, a will is more like a set of instructions for the probate court—it actually guarantees the court will be involved. While a will is absolutely essential for things like naming guardians for your kids, it won't keep your assets out of a judge's hands.

Do I Need a Lawyer to Set Up a Living Trust?

Legally, you can create a living trust using online forms or DIY kits. But from my experience, this is one of those areas where trying to save a little now can cost your family a fortune later. A trust is a detailed legal instrument, and a tiny mistake in how it's written—or more commonly, how it's funded—can make the whole thing useless.

An experienced attorney does a lot more than just fill in the blanks on a form. They're there to provide crucial advice on things like:

Picking the right kind of trust for your specific family and financial situation.

Choosing the best person to be your successor trustee (and a backup, just in case).

Correctly transferring all your different assets into the trust. This is the step where DIY plans fail most often.

Think of it as a smart investment. Spending a bit more for professional guidance upfront can save your family from incredibly expensive and heartbreaking mistakes, ensuring your plan to avoid probate actually works when they need it most.

The whole point of avoiding probate is to prevent delays, high costs, and family fights. The last thing you want is for a technical error in a DIY document to send your estate straight into the court system you were trying to avoid.

And these aren't just hypotheticals. Legal challenges are on the rise. One recent report from Howard Kennedy showed that contentious probate cases and claims against executors shot up by 21% in just one year. A properly created plan is your family's best shield against these kinds of escalating legal battles.

What if I Own Property in Another State?

This is a fantastic question and a situation many people find themselves in. If you live here in Arkansas but own a vacation home in Missouri or a condo down in Florida, that out-of-state property creates a special headache. The main probate in Arkansas won't cover it.

Instead, your family would be forced to open a second probate case in that other state. It's a process called ancillary probate, and it means exactly what you think: double the attorneys, double the court fees, and double the hassle.

A revocable living trust is the perfect tool for this. By simply deeding your out-of-state property into your Arkansas-based trust, you sidestep the need for ancillary probate completely. Your successor trustee can then manage and distribute that property according to your wishes, no matter where it’s located.

We’ve hit on some of the big questions here, but every family’s situation is a little different. For a deeper dive into more specific scenarios, you might find our in-depth Arkansas probate questions and answers guide helpful.

At ArkansasLegalNow, we provide the tools and guidance to help you create a comprehensive estate plan with confidence. Our court-approved forms and step-by-step process make it simple and affordable to protect your family and avoid the probate process. Take control of your legacy today at https://arkansaslegalnow.com.